Sun Pharma Explores Financing Options for $12 Billion Organon Acquisition

- Blog Healthcare Industry New Trending News

- Entrepreneurs Story

- May 6, 2026

- 699

- 11 minutes read

On April 27, 2026, Sun Pharmaceutical Industries Limited signed a definitive agreement to acquire Organon & Co. of the United States, in a landmark deal for the global pharmaceutical industry. The all-cash deal, which is priced at an enterprise value of around $11.75 billion (often referred to as the $12 billion Organon acquisition), is the largest overseas takeover by an Indian pharmaceutical company till date.

It’s not just about size for Sun Pharma. It is a calculated move to enter the high-margin space of women’s health and biosimilars, taking the company into the top-25 global pharma majors. But the key issue for investors and analysts is the complicated “funding mix” needed to finance this multibillion-dollar bet.

Funding the Giant: A Multi-Pronged Funding Mix

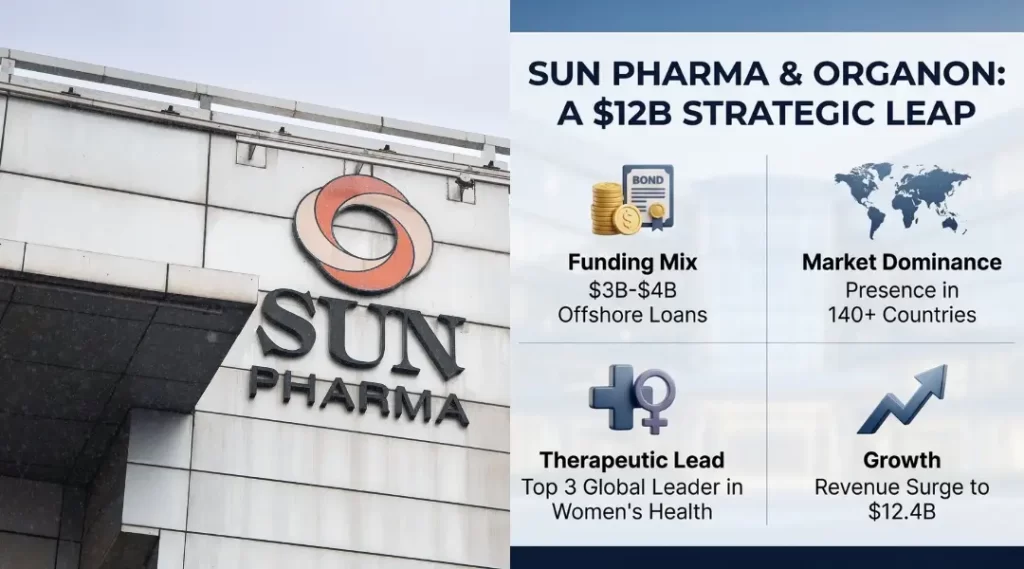

Sun Pharma is looking at a range of financing options to fund an all-cash deal worth $11.75 billion while maintaining its investment-grade credit profile. This sophisticated strategy, similar to a startup’s agile financial planning approach, is designed to replace initial bridge loan facilities with more sustainable, long-term debt instruments.

- Bondholder Exchanges and Debt Restructuring – A big chunk of the funding comes from Organon’s current debt load of about $8.6 billion. Sun Pharma could also offer Organon’s existing bondholders the chance to exchange their existing bonds for new debt from Sun Pharma. The move would help the company to absorb Organon’s debt obligations into its own capital structure smoothly, possibly on better terms.

- Eurobonds – The firm is also eyeing a possible euro-denominated bond issue. The agency said the combined company is likely to have a stronger balance sheet than Organon and that the bonds could be rated one or two notches higher than the standalone rating.

- Big Offshore Loans – Sun Pharma will raise between $3 billion and $4 billion through offshore loans to fund the $14-a-share bid’s immediate cash needs. JPMorgan Chase Bank, N.A., Citigroup Global Markets Asia Ltd. and MUFG Bank, Ltd. are acting as financing banks. Sun Pharma has appointed J.P. Morgan Securities LLC and Jefferies LLC as its financial advisors.

- Use of Internal Accruals – Sun Pharma came into the deal from a position of strength, with net cash positive and approximately $3.2 billion in cash and liquid investments as of December 2025. The company is expected to use $2.0 billion to $2.5 billion of its existing cash reserves in the final funding round.

Strategic Rationale Why Organon?

The $12 billion Organon purchase is a “logical next step” in Sun Pharma’s evolution from a generics-led producer to a global heavyweight focused on specialty products.

- Women’s Health Leadership: Organon is a global leader in women’s health with more than 70 products in its portfolio. With this acquisition, Sun Pharma is now among the top-three global players in the therapeutic area.

- Biosimilars Entry: The deal is a “buy-rather-than-build” blueprint for Sun Pharma’s biosimilar strategy, making the company the 7th largest global biosimilar player.

- Geographic Expansion: The combined entity will have commercial presence in 150 countries after the acquisition, with 18 large markets each generating more than $100 million in revenues. Key new markets are China, South Korea and various emerging markets where Sun Pharma had little presence.

- Revenue Impact: The combined entity is expected to generate annual revenues of approximately $12.4 billion on a stand-alone basis, which is roughly double the current scale of Sun Pharma.

Risks of Integration and Financial Metrics

The strategic fit is strong but the size of the deal poses a huge integration risk across 150+ countries.

- Pro Forma Leverage: The pro forma net debt-to-EBITDA ratio of the combined company is expected to stabilize at around 2.3 times in the near term following the merger.

- Deleveraging Plan: Management is focused on an aggressive deleveraging plan supported by EBITDA and cash flows expected to almost double after the merger. There is no official disclosure of a specific numerical deleveraging target or timeline.

- Synergy Potential: Sun Pharma expects to deliver cost synergies of about $350 million over a two to four year period through procurement efficiencies and optimized manufacturing footprints.

Frequently Asked Questions (FAQs)

What was the cost of the Organon buy for Sun Pharma?

Sun Pharma announced a definitive agreement to acquire all of the outstanding shares of Organon for $14 per share in an all-cash transaction. That works out to an enterprise value of around $11.75 billion for the company.

When is the deal scheduled to close?

The transaction, subject to approval by Organon stockholders and regulatory approvals, is expected to close by early 2027. Internal estimates suggest that required approvals could be secured as early as December 2026.

What Organon adds to Sun Pharma?

“For Sun Pharma, Organon’s world class portfolio in women’s health and biosimilars along with its commercial presence in 140 plus markets would be a great addition. Post acquisition, the combined entity will be active in 150 countries. It also helps to build a big presence in new markets such as China, South Korea.

Will this deal push up Sun Pharma’s debt significantly?

Yes, the transaction will result in a significant increase in consolidated leverage and the net debt to EBITDA ratio is expected to be at 2.3x after the merger. But management is on track to deleverage aggressively, supported by EBITDA and cash flows that are expected to nearly double by close of the transaction.